A year ago, I posted a blog on the remarkable political uncertainty we faced in 2012. This was driven by numerous elections for heads of state which together account for 60% of combined GDP of the G20 countries. Today, what do investors, managers, and consumers know that we didn’t know a year ago? The answer to that question holds huge implications for big decisions to come.

The answer to that question is the focus of our forthcoming conference:

We will hear presentations from Sheila Bair (former Chairman of the FDIC), Dennis Lockhart (President of the Atlanta Fed), Jeremy Grantham (co-founder and Chief Investment Strategist of Grantham, Mayo, Van Otterloo), David Rubenstein (co-CEO of Carlyle Group), Robert Hugin (CEO of Celgene Corp.), Kyle Bass (Heyman Capital) and many others. Tom Keene of Bloomberg Radio will offer commentary. If you have an interest in learning more about the conference, please click here.

The elections and political changes of the past year heighten urgent questions such as these:

· Fiscal Policy: How will the U.S. stimulate its economy and yet plot a course to reduce the overhang of government debt?

· Regulatory Policy: Major sectors of the U.S. Economy have been the focus of new and possibly onerous regulations. Will the results of the election change the investment outlook in these sectors? How do the experts handicap the prospects in various industries and economic sectors?

· Foreign Policy: How will the stance of the new administration affect the presence of the U.S. In international disputes in the Middle East, South Asia, East Asia, and Europe? What does this imply for investing in developed and emerging economies?

· Incentives for Innovation and Business Expansion: Growth remains the major challenge for the U.S. Economy in the medium-term. Will the new administration promote such growth in the private sector? What does this imply for a recovery of venture capital investing and investing in growth stocks?

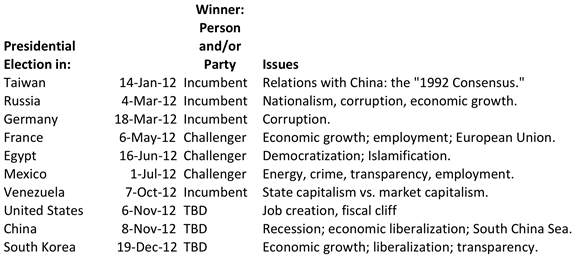

My view is that the election outcomes have generally increased, rather than dampened, uncertainty for decision-makers. In some cases, this is due to the emergence of a totally unexpected new regime. In others, the incumbent regime prevailed, but took policy positions that seem unsustainable. Here’s a brief summary of election results of the year:

Of all the elections this year, two of the remaining elections are of particular impact. The U.S. faces the automatic sequestration of the Federal Government budget in January, the “fiscal cliff” that the Congressional Budget Office says is likely to trigger a recession. The U.S. elections on November 6th will frame the political landscape for addressing this emergency and the longer-term economic challenges. China appears to suffer from economic recession right now, which surely challenges the political consensus there on behalf of economic and political liberalization. Zi Jinping appears to be the likely President-elect there—yet rather little is known of the policies he intends to implement.

And there is more to the landscape of political uncertainty: revolution in Syria; the risk of war between Iran and Israel; the possibility of division and exit from the European Monetary Union. Judging from street demonstrations and the rise of populist movements in various countries, the voters are Very Angry. This alone generates more than a little uncertainty regarding government policy changes and investment climate ahead.

If anything, uncertainty seems greater going into these elections than a year ago. But then again, it is always tempting to believe that “this time it’s different,” and that reversion to the mean will not occur. Yet there is plenty to argue that we are in the midst of regime changes that depart from historical patterns: the world remains in the grip of low growth following the Global Financial Crisis and Great Recession; households and consumers are reducing spending to repay debt; central banks are pursuing stimulative monetary policies and probably cannot push further; governments face enormous debt burdens and are reluctant to borrow-and-spend to stimulate their economies. From the perspective of economic history, this is a dramatic moment.